-

Impostor-ing along

2022 has been my MOST SPENDY year yet. There are SO many things I simply bought on a whim. I kind of regret it, but it also exposed a side of me I didn’t know existed, so I guess I am thankful for it. I thought of myself as a higher being who is not tempted by materialism. I was very wrong. So very wrong.

And the reason I made this list and published it is because I want YOU to know, everyone is FLAWED. Everyone has their INSECURITIES. Everyone has IMPULSES.

IT’S OKAY. As long as you can look at it and be honest with yourself, you’re taking a step in the right direction.

Things I spent MINDLESSLY on –

- Booze. Boy did I waste money on this. I wish I was the sort of person who would regret this expense lol. I’m sure there IS a small part of me, deep deep inside which wishes I didn’t spend as much as I did.

- Knick-knacks. I went on a long-awaited trip to the US to visit my sister this year. I went around buying ALL the magnets I could find because I believed my fridge has an infinite surface area. I bought postcards, I bought some fancy-shmancy coffee-table book and all sorts of trinkets. I don’t even know where most of them went.

- Fit-bit. I forgot the charger in the US and skimped out on the charger here, so now it’s useless.

- Crap I eat. Lordy lord. If my mother sees this post, she’ll probably shudder with an equal amount of anger and disappointment. (Yes, I’m 31, and yes I’m scared of my mom). I have ordered so much food online and paid SO much for food delivery, that I truly believe that industry stands on my shoulders right now.

- This is embarrassing. As an Indian woman, I have A LOT OF body hair and I’m constantly looking at QUICK and EASY and PERMANENT ways to get rid of it. So, on a day filled with whimsy and optimism, I bought a laser-hair-removal-do-it-at-home kinda device. I can’t even recollect its name. I bought it with a lot of gusto six months ago and planned on using it regularly like a good child. And it remains an unexecuted plan.

- Skin care products. Woo-Whee. I did go a little nuts with this. There are just too many things available in the market right now. I don’t know whether to sob or jump with glee. ‘What could you possibly buy?’ you might ask. Here you go – probably bought three or four or five moisturisers (oh who can remember), bought an expensive perfume for myself (which still sits UNOPENED), bought an entire set of hair serum, lip serum, face-wash, toner and all the things needed for a soothing morning routine. How many times have I performed this routine? Oh I could count this in one hand. How do I take care of my skin now? – I do the barest of the bare minimum. I wash my face. Thats all.

I would call the below list – the inbetweeners

- I… bought… an iPhone. I’ve been pining for one for years now and finally my partner talked me into it? Do I regret it? No. Do I love my phone? Yes. Is this the best thing I could have done for my financial health? Nah. Does this sound like I’m trying to convince myself of something? Possibly.

- Clothes. I think I could’ve bought wayyy less? I bought clothes to go to the US and bought clothes in the US. And I don’t even go out all that much. I mean I haven’t bought clothes in years, so I guess it’s not such a bad thing. But man, I really wish I had been a little more mindful about this purchase.

‘Woman, you’re a train-wreck.’ Wait wait. I did SOME mindful spending.

- Health Club membership – This actually helped me streamline and focus on my health for the very very first time in my life. It made me inculcate some semblance of discipline. And now, I’m happy to say, I’ve been swimming almost every day.

- Traveling to the US – Meeting my sister with my mom. Meeting my friends. Spending quality time with them. Well worth the trip. Would do it again.

- Holiday in Goa – Needed this. Desperately.

- Books. Bought twenty-odd books. I was losing my mind a little and needed the distraction.

- Therapy and medication – I was an actual train-wreck in 2021. But 2022, I think I’ve become a more normal human being. Could not have been possible without this.

- Youtube Premium – I cannot stand advertisements. And this is well worth the money.

- WordPress account – Hey! It made this whole website a possibility and I’m glad I did it!

- I’m getting married in 2023! Yup, and spending a fair bit for it. No regrets.

-

Coffee and lists

8 Things you can do in the next 30 minutes that will enhance your financial life

- First things first, DOWNLOAD your banking app on your phone! You need to be able to see your money at a moment’s notice.

- Setup separate accounts for savings/investment and expenditure. I have two accounts, one is an expense account and one is an investment/savings account. At the beginning of every month, I move a certain amount for expenditure from my salary account (which is also my savings/investment account) to my expense account. Figure out something like this that works for you, so you don’t have to go insane with tracking your expenses.

- Open a demat account for your investments! This hardly takes any time. There are so many brokers that offer this. There’s Zerodha (Kite), ICICI Direct, HDFC, Sharekhan. What do I use? I dabble with Kite and Sharekhan. Download the app on your phone!

- Jot down all the expenses you think you have had this month. Then look over your account statement. How right were you? What did you miss? What are your blind-spots?

- Look over your payslip and understand the split. What is HRA? How much tax are you paying? What is your EPF contribution? Are there any other deductions?

- Check your EPF balance. Go to https://passbook.epfindia.gov.in/MemberPassBook/Login and login with your UAN and password. Now if you don’t know what these things are, then I suggest you take this 30 minutes to get to know what the hell is going on here. It’s really important that you have access to your EPF account. Also ensure that you have updated the nominee details.

- List down all your assets. How much is in your bank account? What is the total amount you have invested? How much have you accumulated in your PF? How much gold do you have? What’s that worth? How many fixed deposits do you have? Are there any SIPs that are running every month? What do they add up to?

- List down all your liabilities. If you have debt, then ensure that you are doing everything you can in order to pay it off. Paying back the minimum for your loans only increases the interest rate. So come up with a strategy on how you can tackle this.

-

Let’s go on a date!

Instead of drowning each other while screaming about money or sitting in deafening silence in the fear of talking about money. Let’s try this setting instead, we shall go on a date.

You and your partner gather around a delicious meal, and you’re playing your favourite Lo-Fi music on the side. Both of you look great, and to top it off there’s some light wine to soften the jitters you might be feeling. This might be the first time you’re doing this, so I thought I could help you out by putting down a “fun” checklisty-thing. (ok it may not be sooo fun, which is why we did up the setting SO much).

Appetizer: bring it on!

- What are the exciting things you want to do in the coming year?! – Talk about this with your partner, be honest, so there’s no room for miscommunication and misunderstanding. What do they think of your plans? What are their plans? What do you think of them? Can you support them? Do you think that’s a bad idea? Are you happy for them? Are you tired because they’re just like they were last year? Some examples of what this could look like to start with.

- Oh I want to take up a dance class as a couple!

- I want to join the gym

- I want to visit France and take pictures in front of the Eiffel Tower!

- I want to upgrade my car

- I want to apply for a promotion

- My job is killing me, I want to quit.

- I’m planning to read one book a week at least!

- What’s your BIG vision for life? – Listen this is your spouse/partner you’re talking to. You should be able to share this and voice it out as honestly as possible. Discuss this at length, talk about how you plan to make it possible and what you’re looking for from your partner. Listen to your partner’s goals, see how you can help them achieve it. How do you strategise both your plans TOGETHER and ensure it’s a success? Some more examples, because I never tire of spoon-feeding.

- I want to live in the country-side in ten years and take care of farm animals. I want a peaceful life away from the city.

- I want to quit the corporate life and start something on my own. I want you to help with the finances during this time, because it’s likely I won’t make any money for a year or two.

- I envision us to be a big happy family – I’m ready to take on the responsibilities that come with it.

- I want to be really rich. I will become a C-suite executive in my company, and this is going to take a lot of effort. This would mean I have to sacrifice family time and focus all my effort on my career.

Drinks: Wine, with a side of…

- Where’s all our money going anyway? – What do you spend on every month? This maybe a little boring to talk about especially if it’s basic like… ‘oh come on, we spend on rent, groceries, blah blah, do we really need to talk about this?’ YES. That’s why we added wine into the mix. Because we are getting to, the guilty-spending. What is the thing you’re guilty of spending this month? This year? Ever? What are your regrets when it comes to money? What was a completely waste of money? What was surprisingly useful? What do you think about your partner’s spending habits? Speak up now, it’s the perfect opportunity.

- Now that you’ve had some liquid courage, it would be a great time to talk about DEBT – Especially if you have NEVER talked about this. Use this time to discuss all the debt-related dread that you have for yourself and for your partner. When do you think you’ll be rid of all of it? Or some of it? Are you planning on taking on more debt together? What does that look like for you both? What kind of career changes do you need to make in order to support the growing lifestyle along with the growing debt? Should you ask your partner to stop using the credit card all together? Do they seem to have a mounting credit card problem? Do you?

Main Course: the meaty bit

Ok so you’ve gone through your short term and long-term goals. You’ve talked about spending. What else is there?

- Do your goals have legs to stand on, financially? – If not, how are you going to make it happen. How much is this going to cost you? Say your husband wishes that the child/children to go to the best school possible, and you both know this is going to cost a bomb. How are you both going to make this happen? Is there a middle ground? Can they go to an above-average school for now, while you invest for the next decade to put them in the best possible college/university? Say your wife wishes desperately to quit her job in the next ten years and move to the country-side. Can you support this? Do you think ten years is too short a period? How do you need to plan your career and finance in order to make this happen? Is this even feasible?

- Time to calculate: your combined NET worth – I don’t know why people think only rich people do this. Everyone should do this. While you’re munching on that delicious meal, get a pen and paper and estimate (approximately) what you own and what you owe. Calculate the net worth. OK. Whatever the answer is. It’s all good. You both are on the right path toward melting away that debt or building wealth, or whatever it is you want to do with your money. It may be time to take a very serious look at making some budget cuts or, it may be time to rejoice with yet another glass of wine.

- Before we get to dessert. Let’s get some depressing topics out of the way – Do you both have term insurance? Have you added the nominee details on all your assets? What about other insurances, like medical insurance, accidental insurance etc.? What does your emergency fund look like?

Dessert: get some ice-cream!

- Retirement. What’s in store? – How much do you have saved up for retirement? How much do you contribute to it every month? What does the total look like? Should you plan for your parent’s retirement (check here for more info on that!). How long do you plan on working? Are you enrolled in any government schemes (read more about that here)

Was this a fun date?

Finally, look back at this date and see what you can add or subtract from it. Or perhaps even change it to suit your needs and circumstances. But do this activity every once in three months, just so you know where you stand. And this will also help address how your partner is feeling. If this wasn’t fun, then maybe figure out how to make it so? Get a small checklist and go through it quickly over the appetizers itself. The plan is to ensure both of you are on the same page regarding money and financial goals.

Any leftovers?

So what was missed? Did you not cover talking about how much you want to save every month? Or maybe you forgot to add your travel plans which are coming up next week. Catch up on all the things that you felt wasn’t covered and plan the next finance date now!

- What are the exciting things you want to do in the coming year?! – Talk about this with your partner, be honest, so there’s no room for miscommunication and misunderstanding. What do they think of your plans? What are their plans? What do you think of them? Can you support them? Do you think that’s a bad idea? Are you happy for them? Are you tired because they’re just like they were last year? Some examples of what this could look like to start with.

-

Tough times ahead. Probably.

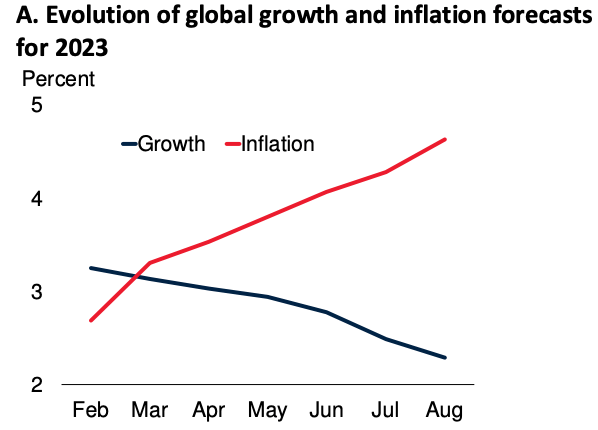

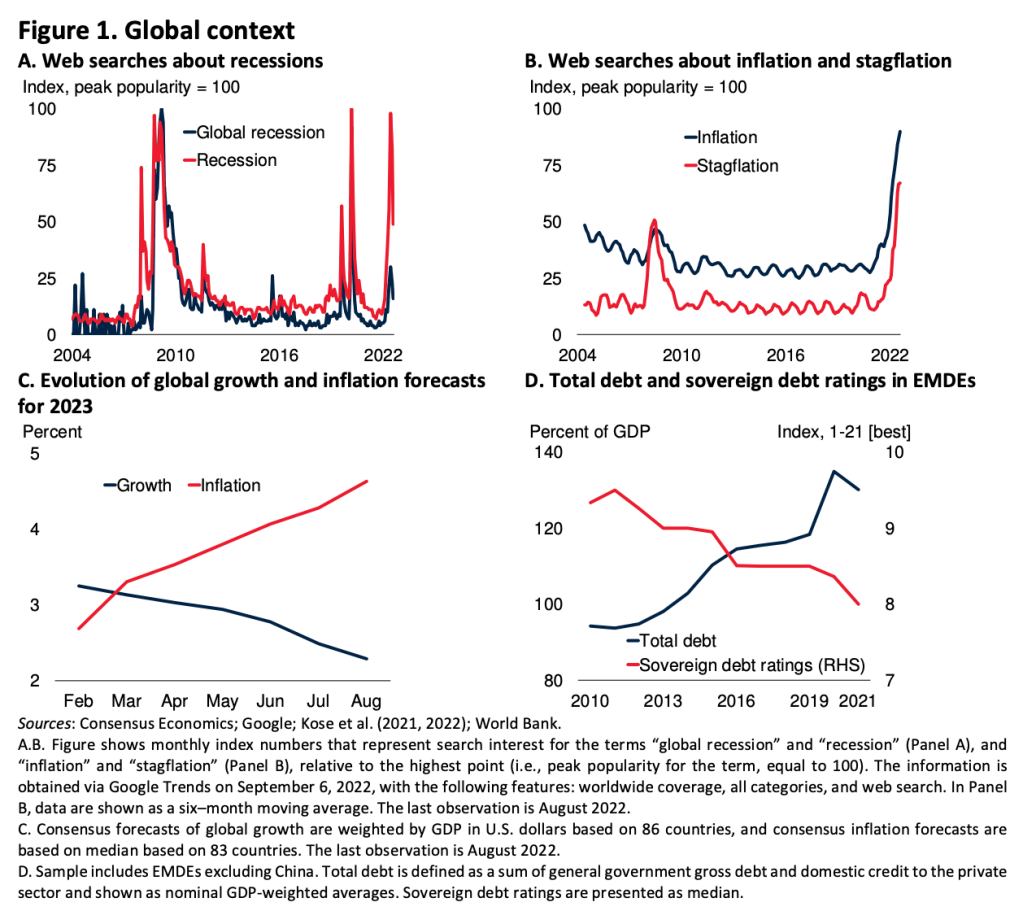

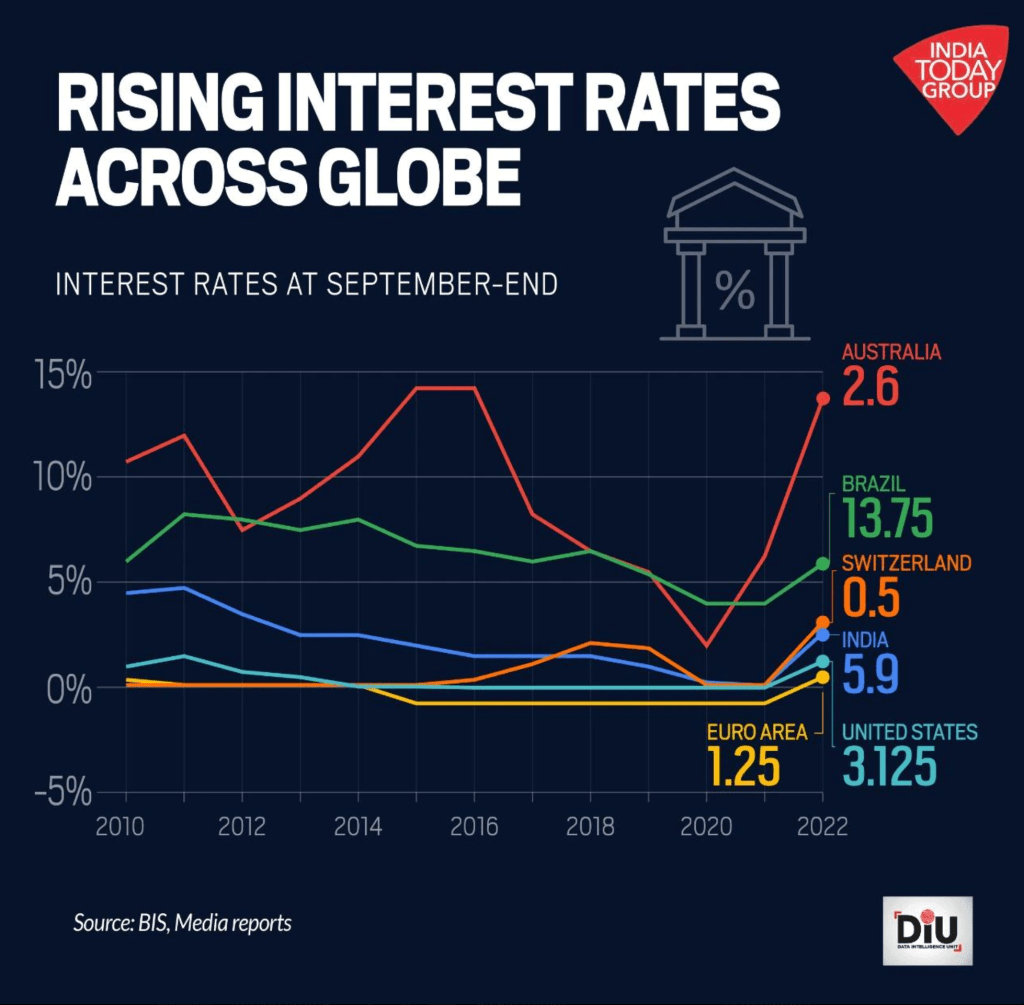

Is there going to be a recession in 2023!? After going through some data, what I can say (and I know very little, so take what I say with a grain of salt) is that the growth is going to slow down for sure, and inflation will probably increase. But recession? On one hand I see that emerging countries are going to face quite the backlash, but on the other hand I’ve read reports that say India should be okay?

[See the data I have collected below for reference]

There’s a very high possibility as economies are literally hanging by the balance. Let’s hope that we do not go into recession the next year and we can weather the storm even if that happens.

There are lot of people (or ‘bros’) who claim that ‘The Market is On Sale’, ‘We can make HUGE profits!’, ‘Recession is a good thing for people looking to invest!’.

While they are not WRONG, and yes the stock market will dip and you can essentially buy shares and mutual funds at a lower rate – That is honestly not the best view of a recession, tens of thousands of people are going to lose their jobs, basic amenities are going to become unaffordable, people’s hard-earned savings are going to be wiped out, people will inch closer to poverty – just to name a few terrible things that might happen.

What can you do for others during this time?

- If you have paid help at home, think about increasing their wages next year. Things are going to get expensive for them as well.

- Try not to bargain with local/street vendors or autorickshaws (unless they’re charging something you KNOW is outrageous).

- Tip a little more generously to Swiggy/dunzo delivery executives, waiters, busboys.

- If you know folks who are unbanked, volunteer to help them open a zero balance account through the Jan Dhan Yojana.

- Most of all, try to maintain some perspective during the coming months. It’s going to be all right. Fear-mongering is NOT the answer.

What can you do for yourself during this time?

- Do not touch your investments. If in need of funds, then I totally understand. But TRY to not sell your stuff when the market is low. You WILL lose money.

- This is a general advice, so again think about whether it actually fits your situation. Since there are so many lay-offs going on, I would suggest you stick to the current role for some time.

- Put off big expenses IF possible. For example – you cannot or should not really put off a surgery that’s been planned. Full disclosure – I’m getting married in Feb and this is a BIG expense. I don’t see how I can possibly put this off since all the preparations have begun already. I guess I’ll have to clamp down on other expenses and see how to go from there. But if you can live without a new laptop/ new phone/ a vacation (like a big one), then it might bode you well to save that expense.

- Do not STOP any investments unless there’s an actual need for that money. Like the investment ‘gurus’ put it – this is actually the time to invest in the market. So if you already have systematic investment plans running, do not stop them. Let them continue.

- Pad the Emergency Fund with more cash. Whatever you think you need if you get laid off, you might just need more given the rate of inflation and the possibility of a global recession. I recently had to use up my emergency fund, and have restarted the painstaking job of building it back up again, honestly, I’m not sure if I can reinstate it back to its previous glory. But I’m going to try.

- Ensure that you are using all the benefits that your employer is providing you.

- Get a term insurance plan. I cannot stress on this enough.

- Just because the CRYPTO market has imploded does NOT mean it’s the time for you to heavily invest your life savings in it. It’s extremely volatile and HIGHLY unregulated. Only only only invest if you’re completely okay with the possibility of losing ALL the money.

Now the data, as promised:

Excerpts from ‘Is a Global Recession imminent?’ – by World Bank Group

As growth is slowing sharply, fears of an impending global recession are rising (Figure 1A). Stagflationary pressures are also mounting as inflation reaches new multi-decade highs in many countries (Figures 1B and 1C).

Moreover, rising global borrowing costs are heightening the risk of financial stress among the many emerging market and developing economies (EMDEs) that over the past decade have accumulated debt at the fastest pace in more than half a century (Figure 1D).

These downgrades in growth forecasts do not imply that a global recession will take place in 2022 and 2023.

However, these forecasts imply that the world economy is set to experience weaker growth next year than it is this year.

But if previous global recessions are a guide, there are still at least two reasons to be concerned about the risk of a global recession in the near term. First, given the current weak growth outlook, even a moderate negative shock could push the global economy into recession. Second, the recent slowdown in global GDP growth reflects pronounced declines in growth in several major economies.

Conclusion: Recent consensus forecasts suggest that the global economy will experience its steepest decline in growth over the next two years following an initial rebound from global recession since 1970.

A global recession would also translate into a sharp decline in growth in EMDEs. In light of elevated vulnerabilities in many of these economies, they would face severe challenges associated with financial stress.

Our analysis indicates that the global economy could escape a recession even if additional monetary policy tightening beyond current market expectations is needed to reduce inflation. However, this would require the additional tightening to be implemented in such a way as to generate an orderly adjustment in financial markets. More importantly, policymakers need to utilize the full menu of options available to get ahead of inflation and reduce the likelihood of a sharper decline in growth.

If the ongoing global slowdown turns into a recession, the global economy could end up experiencing even larger permanent output losses relative to its pre-pandemic trend

Other Publications

https://www.hindustantimes.com/world-news/worst-to-come-2023-will-feel-like-recession-imf-warns-in-world-economic-outlook-cuts-india-growth-forecast-101665500681971.html – “’Worst to come… 2023 will feel like recession’: IMF warns, cuts India forecast”

https://www.thehindu.com/business/recession-unlikely-in-apac-region-in-2023-moodys/article66179117.ece –

“India has emerged as “a bright light” at a time when the world is facing imminent prospects of a recession, IMF chief economist Pierre-Olivier Gourinchas had said.”

”A recession is unlikely in the APAC region in the coming year, although the area will face headwinds from higher interest rates and slower global trade growth, Moody’s Analytics said on Thursday.” -

Things to keep in mind before you buy the thing you think you NEED

- Can it wait a day or two? Most likely, you don’t actually need it. There’s a lot of research that shows that the act of simply adding the item in the cart is more than enough. So maybe you can do that instead of completing the transaction? Let it chill in the cart for a day or two and if you still feel the hankering to buy it, then go ahead! If not… then let it be. Forget about it and move on with your life. You basically ended up saving money, phew!

- How are you going to pay for it? Are you using a credit card? Are you using the credit card to build good a good credit score and add some points or are you buying something with the money you don’t have? Hmm? If it’s the latter, please please rethink your decision. You shouldn’t be buying random things with the money you don’t have. There are several different ways to use the credit card, but the least favourable way to use it is to actually buy things on credit. You do not want credit card debt.

- Do you already have something similar? If this is a pair of shoes you’re buying that looks very similar to the other pair of shoes you bought a month back (and have used like once), then you probably don’t need really need this?

- How much do you see yourself using this? Yeah, so this is another painful way of figuring out cost per use right? Maybe you shouldn’t be paying this amount for a dress if it’s made of bad fabric. The cost/use here is super high. Might as well buy something that will last long, easy to maintain and can withstand a little bit of wear and tear. Go for quality over quantity, and turn your expenses into investments. Boom.

- Where will you keep it? If this is some sad trinket type thing you’re buying to beautify your house, then RETHINK – you need to figure out exactly where it’s going to go before you buy it. Otherwise it’s just going to gather dust and take up space. Of course this example is suspiciously specific because I have done this multiple times.

- and the most important – Why you shopping bro? Why did you open the app? What are you actually looking for? If its something you need then go through points #1 to #5 to really assess that. BUT. If you don’t even know why you’re here and you’re just scrolling through amazon like its instagram, there is a bigger problem here. Ask yourself – What am I trying to do? If you’re just bored then maybe it’s time to take a step back and realise that you have built some dangerous habits that will just cause you regret. Work on distracting yourself from shopping (yes, I know shopping itself is working as a distraction). But we need a distraction from this distraction. Do something else!

-

Worksheets and templates

Personal Finance is PERSONAL. I can write and write and write, but it doesn’t do much without your active participation. Below are some templates I have created that will enable you to get to know yourself a little better. Get comfortable and explore them one by one 🙂 Enjoy!

Goals Questionnaire – Notion

If you want to share your responses with me, then go to this link to fill out the form containing all the same questions below!

LINK – https://forms.gle/h9ePyS9ZkAtukdHU7

Who are you financially? – NotionIf you want to share your responses with me, then go to this link to fill out the form containing all the same questions below!

LINK – Who are you financially? -

Women and money – an introduction

The reason that I thought I should have a separate section to discuss money and women is because, apart from the fact that finance is positioned as a difficult subject to understand – Women have to face extra hurdles and barriers to

- Secure a source of income

- Ensure that the income is competitive

- Assert themselves in a male dominated world/ household/ workspace

- Overcome stereotypes about women being unable to handle or understand money

- Overcome fear and low self-esteem when it comes to money

- Fight people who bulldoze their opinions onto women

- Tolerate endless mansplaining and jargon that is wrapped around money

- Access to simple and easy-to-understand financial education

The rhetoric around money, especially for women is that it is difficult to understand and is steeped with the fear of the unknown. Pepper this with unrecognizable finance terms and we have a woman going deep into her shell unable to move with decision paralysis.

Here are some of the things that I have noticed about women and money –

- We are actually just as, if not more interested in building our wealth when compared to men

- We are resilient investors, not easily upset by the ups and downs of the market. So we make excellent long term investors. (only type of investing I know to be honest)

- We are insane savers. Oooh a woman and her shopping. Pish Posh. We can save like nobody’s business. Scrimping and saving is what we do baby!

Some myths about women and money –

- We are emotional investors. L.O.L. Sure. Women are no different from men. Some are emotional investors, some can be cold and calculating, some are easy-going, some are risk averse. Yes, we come in all shapes and sizes.

- Math is hard. I’m running out of LOLs to give. Again, we are just human beings, not born out of a unicorn on a blood moon day. Some get math, some don’t. But its not a barrier of entry for sure. My math is terrible, but I love finance. We exist.

- We are risk-averse. Yes we are. Some of us are gullible. Some of us are super smart. Some of us love research. Some of us can gamble all night.

All the myths around women and money come from painting a woman and her abilities with a single brush.

We’re not a homogenous group of people who think and operate the same exact way in any given situation.

Some depressing statistics that’ll most likely dampen your day –

Scroll down for India-related data

Excerpts from – https://www.weforum.org/reports/global-gender-gap-report-2022/digest

In 2022, the global gender gap has been closed by 68.1%. At the current rate of progress, it will take 132 years to reach full parity.

Among the eight regions covered in the report, South Asia ranks the lowest, with only 62.3% of the gender gap closed in 2022. This lack of progress since the last edition extends the wait to close the gender gap to 197 years, due to a broad stagnation in gender parity scores across most countries in the region.

In 2022, gender parity in the labour force stands at 62.9%, the lowest level registered since the index was first compiled. Among workers who remained in the labour force, unemployment rates increased and and has remained consistently higher for women.

While the share of women in leadership has been increasing over time, women have not been hired at equal rates across industries.

For frontline operational roles, the overall gender wealth gap amounts to 11%; for professional and technical type roles, the gender wealth gap nearly triples to 31%; and for senior expert and leadership roles it expands further to 38%.

INDIA RELATED STATISTICS

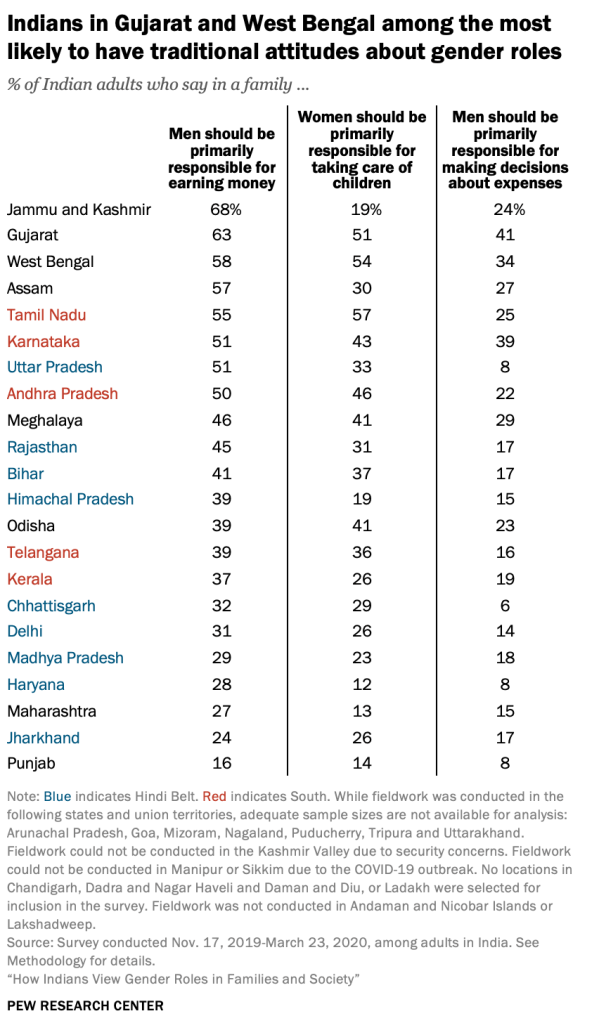

A slim majority of Indians (54%) say that both the men and the women in a family should be responsible for earning money. But 43% instead take the view that men should be the primary earners. Moreover, nearly two-thirds of Indians (64%) – including 61% of women – express complete agreement with the idea that a wife always is obligated to obey her husband. https://www.pewresearch.org/religion/2022/03/02/views-on-womens-place-in-society/

Younger Indian adults typically are no less traditional than their elders in their views on family gender roles, and these attitudes do not vary much between men and women. For instance, 33% of Indian women (along with 34% of men) say that sons should have greater rights than daughters to inherit from parents.

Most Indians say that both women and men should be responsible for earning money (54%), caring for children (62%) and making family financial decisions (73%). Still, substantial minorities have traditional views when it comes to family responsibilities, saying men should be the primary money earners in a family (43%) and women should be the primary caregivers for children (34%). And one-in-five adults say men should be the primary decision-makers about family expenses.

https://www.pewresearch.org/religion/2022/03/02/gender-roles-in-the-family/

Even though most Indians think men and women should share in family responsibilities, nearly nine-in-ten Indians (87%) completely or mostly agree with the notion that “a wife must always obey her husband.” This includes a majority of Indians (64%) who completely agree with this sentiment. Women are only modestly less likely than men to say that wives should obey their husbands in all situations, and most women agree completely with this sentiment (61% vs. 67% among men).

Ending this on this slightly more positve note –

Nearly two-thirds of Indians (64%) say sons and daughters should have equal inheritance rights from parents, including majorities across all religious groups.

We have a very very long way to go. It starts with being aware and taking control of our lives. It starts with becoming financially literate and financially independent. Let’s do this together 🙂

-

What can your country do for you?

Since the UPI has been introduced, I barely carry a wallet, let alone cash when I go out. It has quickly become one of the most used conveniences. I’m sure it’s the same with you lot as well.

While the government may have its ups and downs, it has come up with a few schemes that we should engage with and if possible, disseminate to people who don’t have the same privilege as us.

There are many that help the unbanked and the under-banked. The degree of financial inclusion through them has been wide-spread and is something we should be proud of.

PS: Listen their names are difficult to remember, and the abbreviations confuse me even more. So I’ve just added a phrase before the actual schemes names so you can remember them a little better. For example, the Zero Balance Savings Account is a made-up name, the actual name is Pradhan Mantri Jan Dhan Yojana OR PMJDY (even worse)… cool? Ok. Let’s dive into some of them.

Saving Accounts and deposits:

- Zero Balance Savings Account OR Pradhan Mantri Jan Dhan Yojana –

What is it? – The most important scheme is that which helps the unbanked open a zero-balance bank account. The account is called a Jan Dhan Account.

What can you do? – Check with people around you and see if you know anyone who does not have access to a bank account. This will be a godsend for them. There are a lot of private and public banks that support the opening of a Jan Dhan account. It can be opened with or without an Aadhar card (easier if there is an Aadhar though).

Couple of advantages of opening a Jan Dhan bank account –- Even though the Jan Dhan is a separate type of account, the account will still receive the same amount of savings interest rate.

- Encourages people to use the digital banking service.

Read more about this here – https://www.pmjdy.gov.in/about

How many accounts have been opened using this thing? – As of Mar 2021, its around 42.2 Crore accounts.

How are women doing here? – Around 55% of the Jan Dhan Accounts have been opened by women!- Post Office Recurring Deposit a.k.a National Savings Certificate – Another initiative by the government to encourage low/middle-income earners to invest their money and save tax as well. This is a deposit type thing available in a Post Office and has a lock-in period of 5 years at 6.8% p.a. Even though you can claim this for tax purposes under 80C, the return is NOT tax exempt.

- Double-your-money Fixed Deposit a.k.a Kisan Vikas Patra – Would you like to double your money in roughly 10 years and 4 months? That’s exactly what the Kisan Vikas Patra achieves. This is not a month-on-month scheme but a lump-sum investment. This is NOT tax exempt.

Details of all the post office savings schemes are available here – https://www.indiapost.gov.in/Financial/pages/content/post-office-saving-schemes.aspx

BREAK time. I can’t or shouldn’t keep suggesting my readers to drink beer, maybe grab a crispy coffee? Think about who all can benefit from the above plans and come back to this post.

Insurance Schemes:

- Affordable Life Insurance Cover a.k.a Pradhan Mantri Jeevan Jyoti Bima Yojana – What is this? – This is basically a life insurance scheme for which you need to pay Rs.436 every year. The life insurance cover is for 2L. This is a term insurance plan, meaning you will not receive your premium back or a sum assured if you outlive the term plan.

What can you do? – I have enrolled into this because I found it to be very reasonable and wanted to check out how difficult/easy the process is. If you have access to internet banking, this should take you less than 30 min to setup. There is an auto-debit feature, so just make sure you/ whoever you’re helping has that 436 in their bank account at the time of debit.

Read more about it here – https://jansuraksha.gov.in/Files/PMJJBY/English/Rules.pdf

How many have enrolled in this? – Cumulative count is around 13.11 Crore as of April 2022. - Affordable Accident Insurance Cover a.k.a Pradhan Mantri Suraksha Bima Yojana – This is an accident insurance scheme which will cover both death and permanent disability. The cover for death is 2L, the disability cover is either 1 or 2L depending on the type of disability. The premium for this is Rs.20 per year. Another great incentive that people around you should really be using. There are a lot of families that will benefit from such a scheme.

Read more about it here – https://www.jansuraksha.gov.in/Files/PMSBY/ENGLISH/FAQ.pdf

How many have enrolled in this? – Cumulative count is around 29.01 Crore as of April 2022.

More data on the insurance scheme’s reach available here – https://financialservices.gov.in/sites/default/files/Social Security Schemes June_22.pdf

Yet another BREAK. This is soooo dry people. Look at the picture below to cleanse your eyes and then we’ll get into the next topic.

Pension/Retirement Schemes:

- National Pension System –

What is this? – God this is slightly complex, but let me give it a whirl. This is a way to invest in the market without paying taxes? Not only can you use it for your 80C contribution, the return on the NPS investment is tax exempt as well.

What can you do? – So you can contribute a minimum of Rs.500/month or Rs.1000/annum

Where is my money invested? – this amount can be invested in four different asset classes, namely Equity (max of 75%), Corporate bonds, Government bonds and Alternative Assets like REIT

(What is an REIT!! – Think of it as owning real estate without having the headache of managing and maintaining it).

So the amount invested in each of these asset classes can be chosen by you (Active) or it can be allocated automatically (Auto). Thats all I want to talk about with respect to this. Its really useful, use it if you think it fits you.

Read more about it here – https://npstrust.org.in/content/what-nps - National Social Security System a.k.a Atal Pension Yojana – Would you like to get a regular income of 1000/2000/3000/4000/5000 after you’ve turned 60? This may not seem like a big amount given your age and inflation, but any income during your retirement should always be welcome. You need to pay a certain amount every month for twenty years. The amount you pay will depend on your age and the regular income you want after you turn 60.

Where is my money invested? – The Atal Pension Yojana is invested in different types of asset classes much like the NPS – Government Securities, Term Deposits of Banks and Debt securities, equity and equity related instruments, asset backed securities and money market instruments.

Read more about it here – Atal Pension Yojana FAQ - Public Provident Fund –

I have spoken a lot about this and much more right here – The DREADED PROVIDENT FUNDS. But this is something you should totally capitalize on, anyone can open this, simply through a bank account. Yes, the lock-in period is 15 years, but this a corpus that will grow at a guaranteed and assured rate of 7.1 % (for now).

Should you be taking ANOTHER break now? Go go go! and come back soon!

Schemes for Senior Citizens:

- Social Security for Senior Citizens a.k.a Pradhan Mantri Vaya Vandana Yojana – This is quite the pension scheme for senior citizens looking to get a regular income. Its an insurance + pension plan, in collaboration with the Life Insurance Corporation of India.

So how does this work? You put in anywhere between 1.5L and 15L as a one-time investment. Then the interest is calculated depending on how you want the money to be paid out – monthly, quarterly or yearly. But it’s somewhere around 7.4% – which is GREAT. This is a guaranteed amount you will get.

For example, you put in a one-time investment of 15L and you want a monthly pay-out for the next ten years. The interest is calculated at 7.4% and you end up getting Rs.9250/month for the next ten years irrespective of market conditions. And post the 10 year period, you get your 15 Lakhs back! This is only for people above the age of 60 years. This is NOT tax exempt.

Read more about this here – https://financialservices.gov.in/insurance-divisions/Government-Sponsored-Socially-Oriented-Insurance-Schemes/Pradhan-Mantri-Vaya-Vandana-Yojana(PMVVY) - Senior Citizens Savings Scheme – Similar to the above PMVVY plan, this one also accepts a one-time payment, which can be in multiples of Rs.1000 extending upto a maximum limit of 15L. The interest rate here is also 7.4% which is greater than the FD interest rates being offered by most banks. The only difference here between this and the PMVVY scheme is that this is for a period of 5 years and can be extended for three years post that. This can be availed at many public/private banks as well. Also, this can be used to exempt tax under 80C. The interest is paid out for this quarterly.

Read more about this here – https://www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=62

Schemes for Children:

- Fund for a Girl Child’s future a.k.a Sukanya Samriddhi Yojana – This scheme is one of my favourites. It shows that India is taking the right step in the direction toward woman empowerment and fiscal security. So you can invest in this if you have a girl child below the age of 10. The annual amount for this ranges from Rs.250 to Rs.1.5 L and it also falls under 80 C which is quite nice.

The amount can be withdrawn fully only after the girl child attains the age of 21 or partially (~50%) when she turns 18. The interest rate for this is guaranteed at 7.6% which is awesome. BTW only one account can be opened per child and two accounts can be opened per family.

Read more about it here- https://www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=89

The bar of entry for these plans are quite low which encourages people from under-privileged backgrounds to save for the long-term. The returns for them are solid and backed by the government, which is also a huge plus point. They may even weather inflation and provide a sense of security. If I have missed out any schemes, let me know – I have tried to aggregate almost all the information in one place and provide a bird’s-eye view. I enjoyed writing this article because it made me feel like there’s a LOT to capitalize through the government, and gave me some hope for my country.Most important point – whether you are opening this for yourself or helping some one else, ENSURE that the nominee details are updated. Otherwise your folks will have to run from pillar to post to claim what’s theirs.

- Zero Balance Savings Account OR Pradhan Mantri Jan Dhan Yojana –

-

Traversing retirement with the parents

How to plan for your parent’s retirement?

Listen, this is a mammoth task you’re taking on, so kudos to you 🙂

I helped my mother plan her retirement, I have to say, that was my ONLY contribution – I streamlined it a little and added some structure to it.

So where do we start with this?

Make sure you have their full consent before getting on this journey. If they don’t want to share the details, then reassure them that you’re always there to help and STOP. Do not push them just because they’re your parents.

Fiiiiiine I have their consent, now can we get started? Yes!

If you’re Indian, we both know that our parents are going to play their cards very close to their heart. Not because they’re diabolical beings, but because it’s highly likely we will be treated with kid gloves, especially when it comes to sharing the liabilities.

Its a graceful balancing act… you’re doing this so they don’t have to worry about their retirement. And they’re protecting you so you don’t have to worry about their liabilities. And round and round we go!

ALL RIGHT. After all the see-sawing. Let’s get into the meat of this activity.

Firstly, gather all their assets on one side and all their liabilities on the other side. What does THAT mean? Okay I’ll show you below, its not an exhaustive list but it should be enough to get you started.

Assets:

- Bank Accounts – How many do they have and how much is in them?

- Deposits – How many FDs/RDs do they have? Where are they?

- Provident Funds – If they are working parents, then they will most likely have an Employee Provident Fund. Also, check if they have a Public Provident Fund. How much is in them?

- Gold/Silver – Where is being stored? How much is it worth? Do they also have Gold bonds/ETFs?

- Insurance Vehicles – Back in the day, our parents were sold many ‘insurance investment schemes’ – look for this very thoroughly. They might own schemes that are basically a ripping them off wildly or are DEAD investments. **ENSURE they have very well-rounded medical insurance cover. If they don’t have it, get it ASAP. Additionally, if your company provides medical insurance, check if you can add your parents there as a nominee.

- Shares/Stocks/Mutual Funds – Where are their Demat accounts? What are they? Can you ensure that your parents have full visibility of them?

- Property – They might own land or might have inherited land. Ensure all the documentation for that exists and see if you can ascertain their worth

Liabilities:

- Mortgage/ Home loan – How many years left of this? How much is being spent monthly on this? How much is left?

- Car/Vehicle loan – Same as above.

- Business related loans – Same as above.

- Education loan – Same as above.

- Credit card debt – Same as above.

- Borrowed money from friends/family – How much?

Gathering this data will be illuminating and give you a very clear picture of your parent’s financial health and their success in retirement.

- Put all this information that you have collected in one file that you can refer to.

- Try to ensure that you can make all these accounts and data available on their phones.

- Teach them how to access it and how to track their assets and liabilities digitally.

Go take a break, this would’ve been an insane ordeal. Have a beer and chill for some time. Come back to this with a fresh pair of eyes.

At the end of this exercise, you need to be able to clearly state your parents’ net worth (difference between asset and liability) and exactly where their assets lie.

Okay done, I have a clear idea of what’s what and what’s where… Awesome. When you are sharing this information that you have learned, ensure you do it with great care and sensitivity. Give them confidence about their future through your sincerity and reliability.

Now you know their net worth. How to determine if they are SET for retirement?

Well, it depends on the data that you have gathered.

Let’s do the below exercise and distill it even further –

- What is the net worth? This can be calming, alarming, disappointing, overwhelming. But the point here is to be aware so you can take some informed steps. So yeah… chill. It’s okay. The number was already there before you found it.

- What are their month-on-month expenses? Talk to them. Are you or your sibling a part of their expenses? You must have gotten an idea of this when you have gone through their liabilities, so you already know most of what their monthly obligations are.

- How many more years do they plan on working? My mother is 60 and still works and plans on working for the foreseeable future. Please be sensitive when you’re trying to gather this information.

- Is there a passive source of income? Such as a rental? Is there a way for you to set this up for them somehow?

- What do their short-term expenses look like? Do you have a brother in the United States that they need to visit every year? Or are you planning on relying on them for your wedding or education or seed money for your start-up?

- How much do you plan on supporting your parents during their retirement? If you do have plans of doing so, then using the information from #2 and #3, figure out how much and how long you need to invest in order to make this happen. If the amount you come up with is not viable, plan on investing an amount that you’re comfortable with for now. Keep in mind the number that you would actually need and let it guide your future investment actions.

Throughout this process, I urge you to be patient with your parents and let me reiterate, maintain complete transparency and make sure they have full access and visibility to the wealth they have built.

-

Moving forward

The feeling of being stuck and unable to make lasting changes in your habits is all too real. I have gone through this and have been going through this feeling for over a year now. Of course, this is with respect to health. I’ve been trying to become healthier but its almost an impossible task, because I have the attention span of a goldfish. I need to see immediate results when it comes to health. And it just doesn’t work that way when we’re aiming for long term results.

I still very much struggle with my health especially because of my eating habits. I follow a random diet that is too restrictive and then I binge like there’s no tomorrow.

The key to my health, I have come to realise is – sustainable habits.

Easier said than done. However, I have implemented this for my finances. I don’t look at my portfolio every week or even every month. I only check it around once in three to four months. The remaining time I just put my head down and do the work. Consistently keep putting away money for investing and forget about the results. Just keep repeating the action, till it becomes a part of your routine and yields nothing but the satisfaction of having completed the action itself.

I don’t think about the health of my teeth every time I brush it, I just do. Blindly. The benefits are unseen but the drawback of not doing so is very very evident. Similar to managing health and wealth. These need to be habits that we need to inculcate into our lives.

I’m still trying for the millionth time now, to change my diet and get to a place where healthy eating becomes a habit and not something that needs to be observed and monitored. Until that time, I need to be mindful of what I eat, when I eat and how much. And most importantly, eat when I’m hungry and not to satisfy some weird craving my brain comes up with.

Just putting this delicious blueberry pancake here while we talk about diets, because why not.

It’s a commitment that we need to make to ourselves when it comes to building any habit. Take it one day at a time, and find joy in simply completing the habit for that day without having any expectation of its yield. I find a lot of satisfaction when I save money, and I’m sure my future self is very thankful for all the work I’m putting in now. The feeling of saving and the exhilaration I feel when I spend money are two entirely different things.

It is difficult to describe, but I’m going to try.

It’s the difference between cooking your own meal and enjoying it Vs ordering yummy food online and devouring it. One takes time, but is still a pleasurable activity, the other gives you the dopamine instantly.

It’s like working out and becoming fit to look good Vs putting on make up. No shade on either, I’m just trying to illustrate the differences clearly.

It’s like trying to find a conversational icebreaker in a social gathering Vs using alcohol as a conversational lubricant. Again I have used the latter multiple times, I’m just trying to show how executing these tasks leave you with different feelings.

The former examples here are more difficult, and need more work and control from your side, but leave you feeling more fulfilled. The latter are pleasurable and there’s absolutely nothing wrong with them, however, they are easier and get you quicker but short-lived results.

Creating a habit is hard – especially for the ones that we REALLY REALLY want to achieve but are scared of. So we tell ourselves stories of our potential, shielding ourselves from ever even trying to attain our goals. The fear of failure and rejection has real consequences.

My go to advice here is to START small. Think of one thing that you want to be doing and how you can take one step toward making it happen. Lets see an example.

- You want to start investing, but you’re scared of it since there is SO much to learn about and you don’t know where to even begin.

- Start with index funds! too much? Okay, open a demat account.

- Too much? Okay, google Demat Accounts. Thats all.

- Tomorrow, open the demat account.

- Give yourself a break for two days… tell yourself that you’ve done a good job and then move 500 into your demat account.

- Next day, invest the 500 into the index fund.

If you need help with your financial goals or need help breaking them down like above – then reach out to me through Calendly. Let’s tallk!

- You want to start investing, but you’re scared of it since there is SO much to learn about and you don’t know where to even begin.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.